All over the world, the phase-down of conventional HFCs in food retail applications has become the center of attention in the effort to combat climate change. Most recently, at the meetings of the parties under the Montreal protocol in Dubai where qualitative global phase-down of HFCs was agreed with a target of quantifying the details in 2016.

With the implementation of refrigerant regulations in Europe and the US, the quest for alternative solutions is accelerating. From ugly duckling among refrigerants for food retail applications, CO2 is emerging as one of the most viable and efficient solutions among natural and synthetic refrigerants – not least due to its outstanding COP in trans-critical systems with heat reclaim.

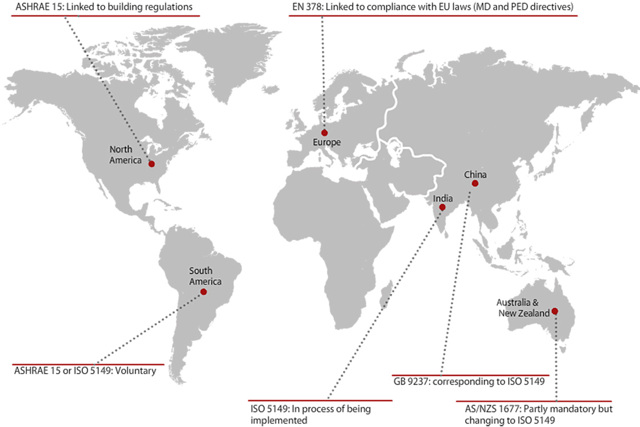

In this article we will explore the regulation surrounding the use of refrigerants in different parts of the world, a development which has brought CO2 to the forefront of attention among global retailers.

Facts and Graphics

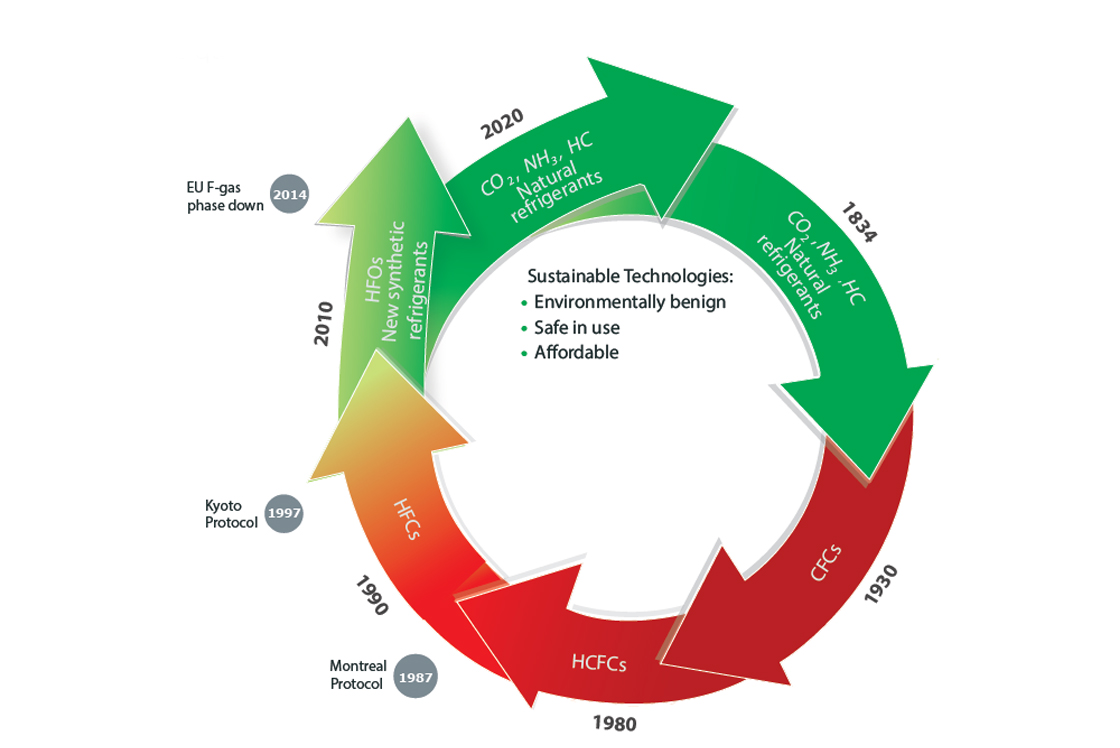

Figure 1: After 180 years of commercial refrigeration, the use of refrigerants has come full circle. Natural, low GWP refrigerants such as CO2, ammonia and hydrocarbons are back as the backbone of sustainable, high-performing and safe solutions.

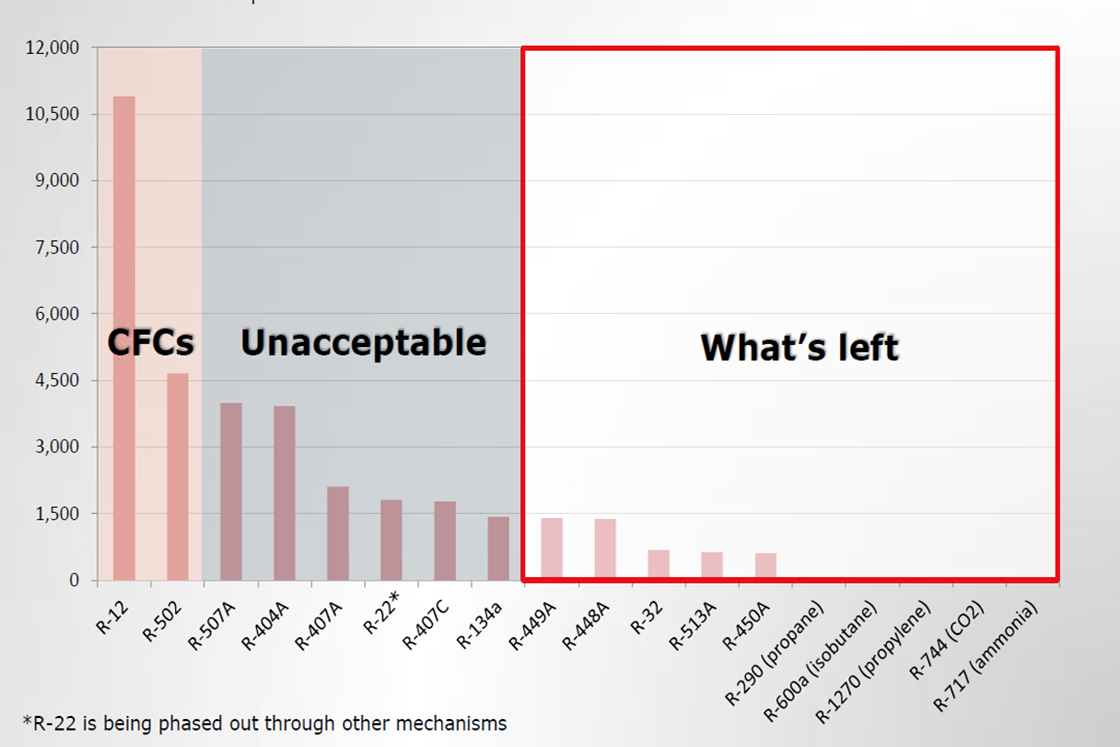

Figure 2: The Global Warming Potential (GWP) of different refrigerants.

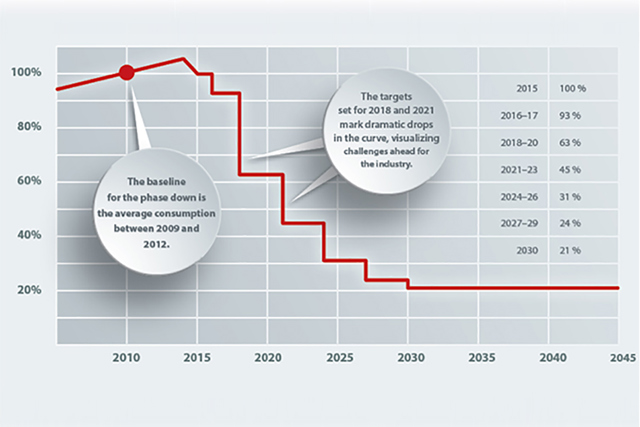

The phase-down of HFCs in Europe started when the F-gas regulation became effective on 1st January 2015. The regulation implies a phase-down of high-GWP refrigerants from 2015 to 2030 by means of an intricate quota system and sectorial bans on refrigerants like HFC. This means that only 63 % of the HFC volumes available today will be available in 2018, and consequently, prices are starting to rise.

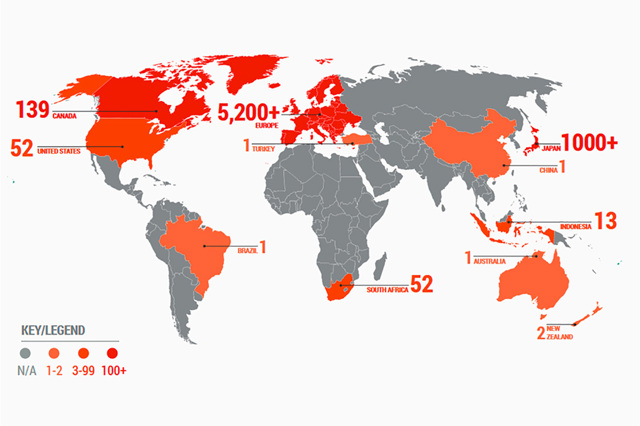

By 2021, the European F-gas regulation will ban R404A from most supermarket applications. The response of the industry has been fast, and at the time of writing an estimated 7,000 + supermarkets are already using different kinds of trans-critical CO2 systems for refrigeration.

Every day, progress is made by the industry to invent components and configurations for sustainable and viable CO2 refrigeration; not only in cold climates where heat reclaim has proved to provide an excellent business case, but also in warmer climates where the energy efficiency of CO2 systems is constantly improved by new technology.

When it comes to CO2 trans-critical systems with heat reclaim, we have only seen the tip of the iceberg. European retailers are experimenting with forward-thinking solutions that not only cover the heating demand of the supermarket itself, but also export heat to local district energy grids. The obvious advantages of solutions like these are fast payback times, typically under 2.5 years, and reduced carbon footprint of the supermarket.

In the US, an array of regulations from the US Environmental Protection Agency (USEPA) on allowable refrigerants and from the US Department of Energy on equipment energy efficiency performance, are fast reducing the technology options left open for manufacturers.

The Significant New Alternatives Policy (SNAP) program governed by EPA seeks to phasedown HFCs over a short period of time. The purpose of the program is to allow a safe and smooth transition away from ozone-depleting compounds by identifying substitutes that offer lower overall risks to human health and the environment. As soon as 2016, high GWP HFCs like R404A will be banned from certain important food retail applications in the US.

In the light of this trend, CO2 is emerging as a preferred refrigerant for supermarket applications. From a limited number of trans-critical systems today, the development of trans-critical solutions is expected to take off during 2016 when the American retailers embrace the opportunities of CO2.

Figure 4: Inspired by the rapid implementation of CO2 as the preferred refrigerant in food retail, the use of trans-critical refrigeration is expected to grow rapidly in the US after the implementation of SNAP regulation. Source: Accelerate America, Shecco, August 2015.

The first phase-out initiatives concerning the ozone depleting substances were regulated through the Montreal Protocol from 1997. Today, the Montreal Protocol still governs the use of refrigerants in many countries. Attempts to renew the regulative framework under the protocol have met resistance throughout the last decade resulting in regional initiatives such as the F-gas regulation in Europe and SNAP in the US.

2015 saw a global break-through in the modification of the Montreal Protocol, when the signatory parties of the Protocol established a formal contact group on the inclusion of HFCs under the substances controlled by the Montreal Protocol. It is expected that this international agreement will use the expertise and the institutions of the Montreal Protocol to phase down the production and consumption of HFCs on a global level within a foreseeable future.

The detailed plans and agreements are expected to be finalized in 2016, sending a strong signal to the industry to keep on developing high-efficiency low-GWP solutions.

2015 also saw two other important initiatives related to the increasing use of low-GWPs, i.e. the Global Refrigerant Management Initiative (GRMI) and the Refrigerants Driver License (RDL). Both initiatives aim at strengthening the technical competencies required to up-scale the implementation of low-GWP solutions.